With the end of the first (and perhaps only) Cameron government in the offing, it is a good time to ask, how has the UK economy changed over the past five years? To what extent has the coalition reformed the UK economy so that it is less prone to instability, of the kind caused by the financial crisis?

The UK’s reliance on the financial services industry made it particularly prone to the effects of the crisis and yet little has been done to change this. There are those, of course, who argue that the benefits that financial services bring to UK plc outweigh the costs or the risks. But the evidence for this is highly questionable.

Plus ça change

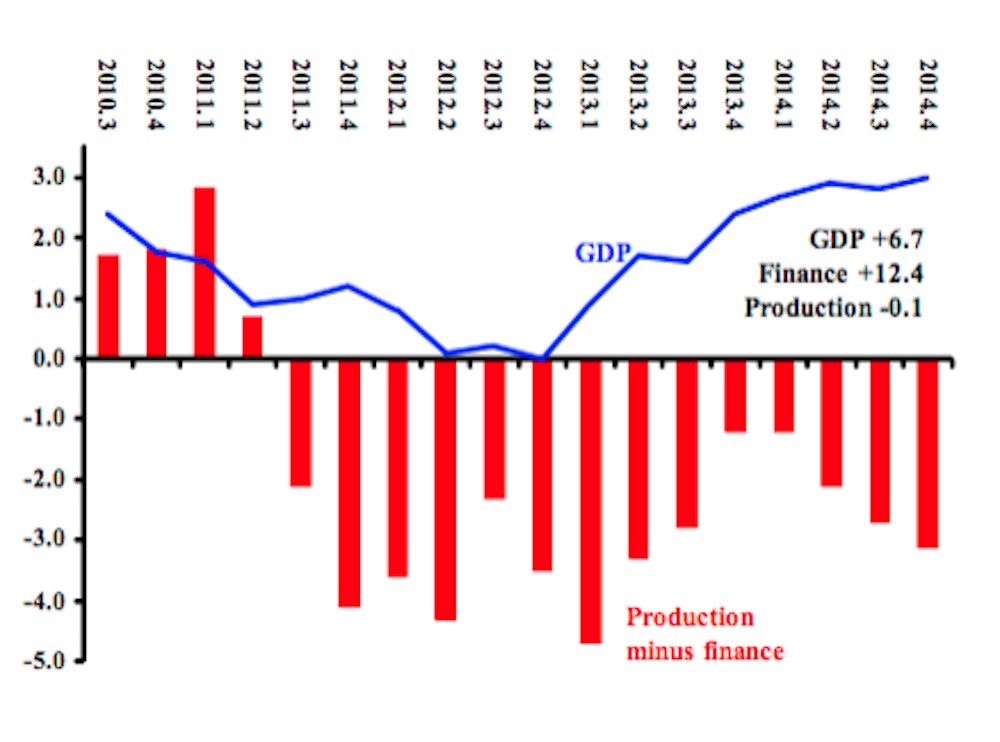

A look at the numbers is not reassuring – the UK remains heavily dependent on financial services for much of the country’s growth. The chart below illustrates this – the blue line shows the rate of growth of GDP, measured as percentage change in each quarter compared to the same quarter a year before. Recent increases have been celebrated by the incumbent government and their cheerleaders in the media.

The red bars, however, measure the difference between the rate of growth of what the Office for National Statistics defines as “production” and the “financial services”. For the first four quarters, “production” grew faster than “finance”. In the subsequent 14 quarters the reverse was the case, finance grew faster than the production sectors (on average 3 percentage points faster). For the calendar year 2014, finance grew at 4%, more than double the rate for production sectors (1.6%).

As a result of this growth pattern, at the end of 2014 overall GDP was about 7% above what it had been when the coalition took office. Over the same period financial services grew by 12.4% and production sectors slightly declined. During the current parliament, finance increased its dominant role in the UK economy, while production – and especially manufacturing – have been treading water.

Finance lowers our taxes?

There are those who like to maintain that the financial services sector, “the City”, is a cash cow for government. Any attempt through government policy to limit the growth and role of the City would undermine public revenue, requiring higher taxes on households and non-financial corporations (an argument partially supported in a 2012 study by Oxford Economics).

Should we all thank David Cameron, as well as Tony Blair and Gordon Brown before him, for keeping our taxes low by facilitating the growth of the financial sector? A fact check provokes serious scepticism. An annual government publication on the City of London reported that financial services contributed almost £66 billion to the public purse in 2014. This amount would represent more than 10% of total public revenue. Though often cited, this number exemplifies the famous cliché, “lies, damn lies and statistics”.

The City of London’s annual report divides revenue into “taxes borne” and “taxes collected”. The latter category accounts for more than 60% of the total tax claimed, £40.8 billion. It consists almost entirely of payments by employees (PAYE and national insurance contributions).

No other sector of the private economy includes taxation of its employees as part of the companies’ contributions to public revenue. Personal taxes are by definition the contribution of the employee, not the company (which is only the vehicle for collection).

Were the financial services sector to shed its entire UK labour force and move elsewhere, most of those employees would in due course find employment in other sectors. The re-employed workers would continue to make their contribution, though the financial services sector had disappeared. Yes, financial services employees pay tax, but so do all others, unless they are non-doms.

What the companies pay

When calculating contribution to public revenue it is only commonsense and sound economics to attribute to financial services only the taxes paid by the companies. Looking in detail we find that the value added tax and employer national insurance contributions make up almost 70% of taxes paid by financial services companies. Of the remaining 30%, corporate taxation is 21% and 9% comes from the “bank levy” (the 0.156% tax on bank-held debt, raised in the latest budget to 0.21%).

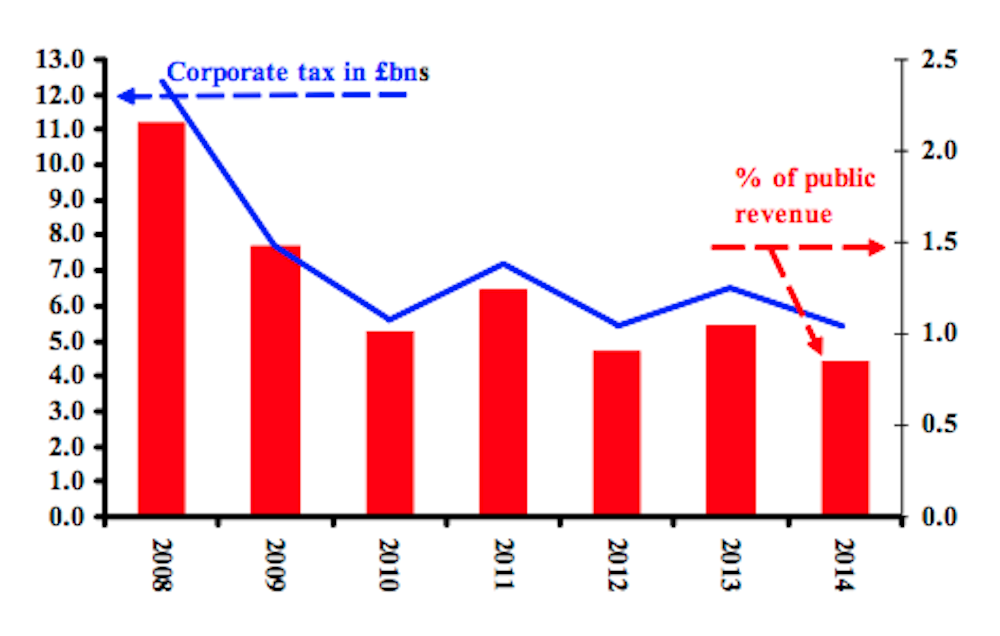

In 2012, the last year for which detailed statistics are available, the £5.4 billion in corporate tax was 2.3% of the reported total income of the financial sector and 4.9% of value added (wages, profits and interest income). The chart below shows rather unimpressive share of corporate taxation of finance in public revenue since 2008.

During 2008-2010 the corporate tax paid by financial companies declined sharply, from over £12 billion to less than £6 billion. In 2014 the corporate tax was less than in any previous year, despite the growth of the sector shown in the previous chart. As a share of public revenue, financial sector corporate taxes fell from a not-very-impressive 2.2% in 2008 to a barely there 0.9% last year.

Despite this rather modest contribution to corporate tax revenue and the singular lack of enthusiasm of UK banks to make loans to the productive sectors of the economy, the lords of finance in the UK would seem to have friends in high places. The coalition government has supported numerous City-friendly policies, including vetoing EU measures to limit speculation by banks in 2011 and banking regulation has been reformed with reticence.

But should this surprise us? Four years ago the Bureau of Investigative Journalism revealed the extent to which the Conservative Party is financed by the City of London – it was the source of more than half of the party’s donors. This year it emerged that almost half of the wealthiest fund managers in the country are Conservative Party supporters.

This City bankrolling of the Tory party makes the frequently cited union contributions to the Labour Party seem modest (details on all party donors is available on the website of the Electoral Commission). It should also make us question further the Conservative Party’s claim of having a long-term plan that will build a stronger, healthier UK economy.