In a recent paper we modelled the likely future supply limits of fossil fuels, and when we might expect to reach “peak” fossil fuel.

Our “best guess” was that global fossil fuel production may peak as early as the mid 2020s, driven by the peaking of coal production in China. We argued that this will increasingly make alternative energy (renewables and nuclear) a strategic pathway for Chinese energy and economic security.

In turn this may see China pressuring for increasing global emissions reductions to boost exports from its alternative energy manufacturing industry. This could tip the balance in future international climate negotiations.

In Australia the story is very different. Domestic oil production is collapsing. However, gas and coal resources are abundant enough to service strong export growth past mid-century (although not enough to provide for China’s future energy demand).

The Chinese case exemplifies that action on climate change can be a “no regrets” policy when it complements efforts to improve energy and economic security – that is, when a policy helps deal with all three challenges. Because their fossil fuel reserves have or are peaking, both the EU and China will improve energy security by switching to domestic alternative energy production. They will also improve economic security by avoiding economic leakage through large energy imports.

With our large coal and gas export industries the immediate “no regrets” options for Australia might seem elusive. But Australia needs to prepare for a possible tipping point in alternative energy production, and global climate agreements that may affect our coal and gas exports.

Australian fossil fuel resources

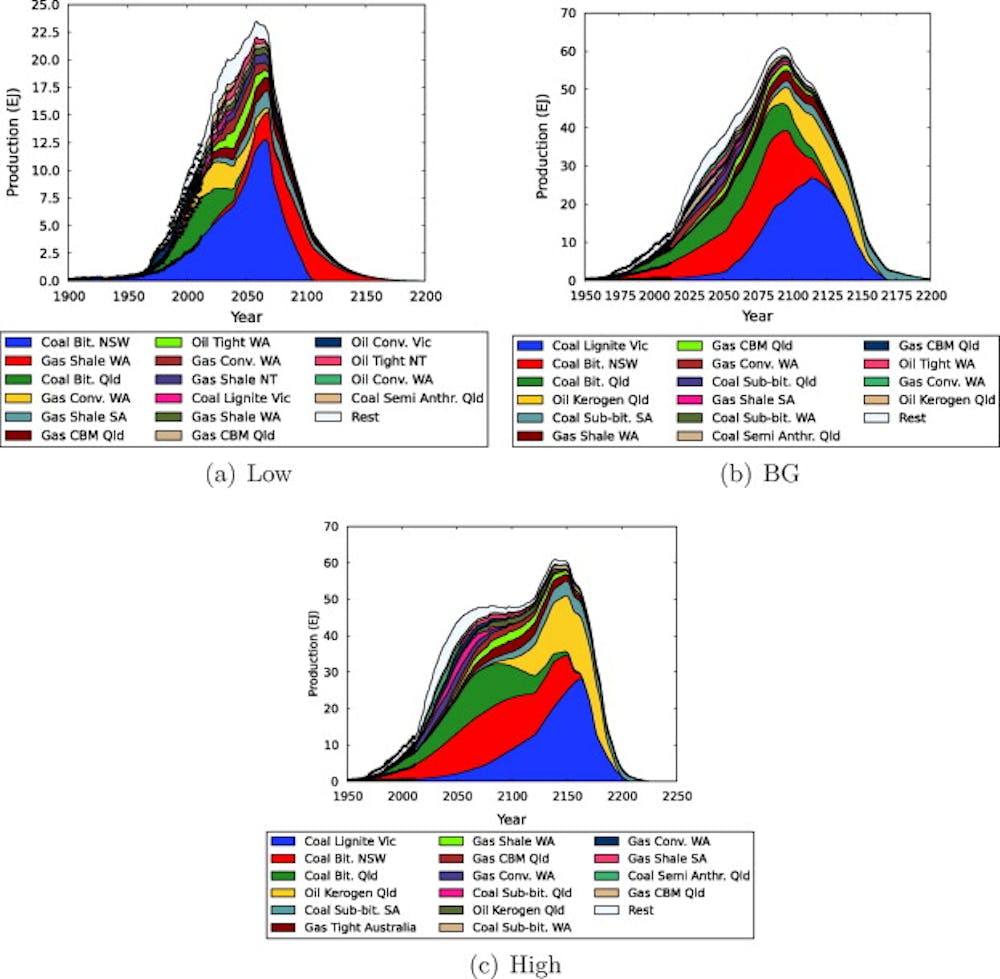

Our work has looked at the geological limits to fossil fuel production assuming no global action to limit emissions and no breakthroughs in alternative energy technologies.

Obviously people are working hard on both of these important issues so consider our modelling below as an upper limit of what Australian fossil fuel resources are capable of rather than a forecast of actual production.

Summing up Australia’s fossil fuel resource availability:

Oil – Poor. Domestic conventional oil production has peaked and we are increasingly import dependent. The growing scale of imports mean that we are basically selling coal to buy oil. Alarmingly, Australia also lacks adequate short term stocks to ride out supply disruptions.

There are substantial kerogen oil resources in Queensland but these are unconventional and are at the expensive and emissions intensive end of the spectrum. Production is currently at the demonstration plant level, so any production of such oil would be starting from a standing start and could take decades to grow to appreciable scale.

Gas – Good but no longer cheap. We have enough conventional and unconventional resources to support a growing LNG export sector, provided international gas prices remain strong. Domestic prices are likely to increasingly reflect international prices.

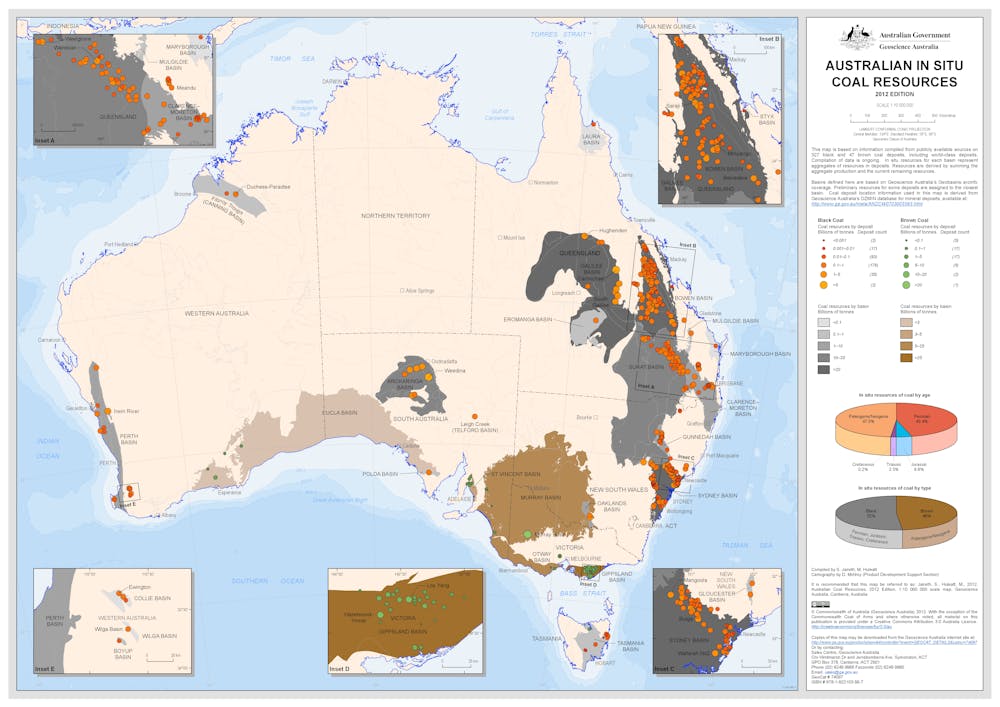

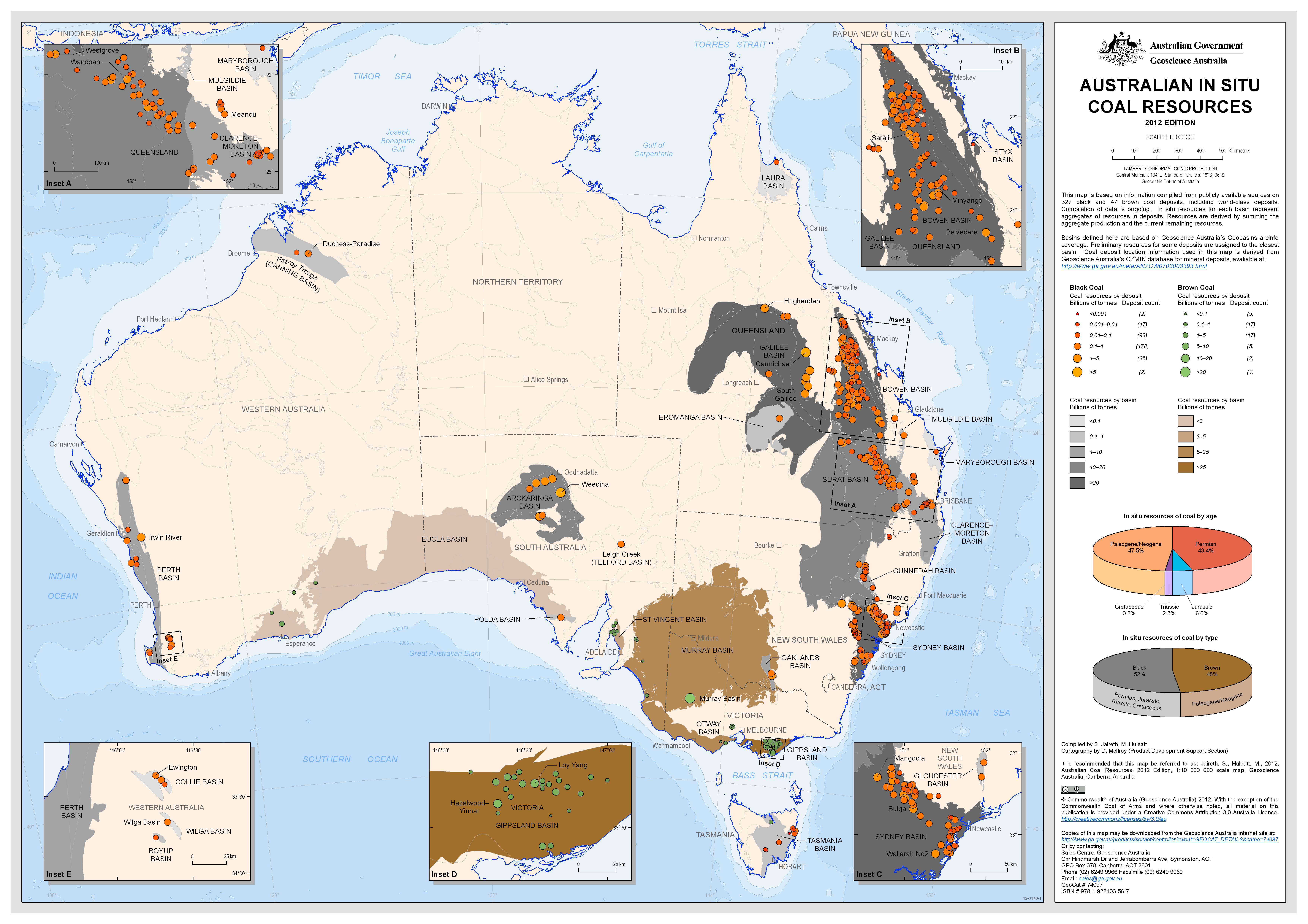

Coal – Abundant. There are enough black coal resources in New South Wales and Queensland to support export growth of this dominant export commodity for another few decades and the vast brown coal resource in Victoria has barely been tapped.

These assessments are purely of the resource scale and do not involve an assessment of local impacts to communities, land, air, water that must also be integral to extraction approval licencing.

{kind=link}

Coal puts Australia in a tight spot

The strategic situation for Australia in terms of energy and climate is complicated by the abundance of our low cost coal reserves. These not only provide the bulk of low cost (provided emissions are not considered) power in our electricity network, but along with gas form the basis of two significant national export sectors.

The poor progress of carbon capture and storage technologies on delivering a low cost, workable and safe way to eliminate emissions from fossil fuel power stations means that the growth of coal and gas would seem at strategic odds with efforts to reduce carbon emissions.

To Australians then, climate action equals a cost to energy and the economy. This makes it challenging to develop policy with the full support of the Australian public.

We should be kind to each other in this ongoing discussion. There are strong and legitimate arguments from those that prioritise climate action and those that prioritise national energy and economic security, neither of which are likely to disappear in the short term.

Developing a bipartisan strategy for Australian economic, energy and climate security will be difficult if we continue to focus on areas that are trapped in this strategic “climate vs economy” conundrum. To get anywhere requires long term policy commitment that will last through successive governments of all persuasions.

To try a different path, we’ve used our knowledge of Australian fossil fuel reserves to suggest four “no regrets” policy areas that can benefit climate, energy and economic challenges all together.

1. Become a leader in smart transport

Australia’s dependence on the private passenger car is now a strategic economic, energy and climate security weakness and will cost us in the ballpark of A$1 trillion in car and oil imports over the next 10 years.

This economic leakage is reducing GDP growth by 4.5% with a subsequent opportunity cost of approximately 500,000 jobs across the economy.

Australia could and should be a leader in dramatically reducing car and oil imports. One technology that can do this is driverless electric cars. Companies such as Google and Uber are vying to be the first to offer a low cost driverless transport service that can give you better service than the private car.

Electricity is a lower cost and more easily managed energy source for driverless transport, so driverless share cars will likely drive the rapid uptake of electric vehicles.

Along with a railway backbone for high density corridors and longer trips, this could reduce car ownership and oil consumption (and hence imports) by up to 90% and lay the foundation for emissions reduction through low-carbon electricity.

2. Greener mining

The long term future of Australia’s coal export sector is fundamentally uncertain at this point. If China manages to pull off its alternative energy switch, they will lay the technology and industrial foundation to replace our export markets, or at least crash the price by providing a low cost alternative.

It’s not helpful to see this as a debate between coal v cleantech (cleantech includes renewable energy technologies and accompanying technologies such as smart grids, electric vehicles and energy storage). Strategically-speaking, it would be better to look at what value cleantech can add to coal and other mining activities.

At the moment much of the revenue received from mining bounces back out of the country again to pay for oil and technology imports – much of it used to conduct the mining process itself.

By greening the mining supply chain (for example through biofuels, automation, electrification with renewable energy, greener explosives) more of the costs can be captured locally, supporting both mining supply chain and cleantech industry development.

This could be supported through the federal government’s Mining Equipment Technology and Services Growth Centre. Strategically this means a higher national return from any future coal and other mining exports, and a guarantee that it supports cleantech industry development.

If we are smart we will use the international market connections and knowhow of our mining sector to support cleantech exports, which will become increasingly essential if export coal demand crashes.

3. A renewable gas target

The current renewable energy target is really a renewable electricity target. This neglects the long term future of Australia’s gas network and misses opportunities for agricultural regions to enter into the Australian energy sector.

A renewable gas target would represent a strategic plan to develop Australian biogas technologies and agricultural energy supply chains in regional Australia. It would also support consumer choice for gas as a renewable energy option, especially in distributed tri-generation.

Connecting renewable gas targets to unconventional gas projects would ensure better regional value-adding and the processing infrastructure for a continued regional biogas industry that endures long after local gas wells have gone into decline.

4. Doubling energy productivity

Improving energy productivity is an essential part of increasing economic productivity and improving energy security.

Australia is falling behind on improving energy productivity. By contrast, the USA has adopted a target of doubling energy productivity by 2030.

Increasing mandatory energy efficiency standards make the job easier for the consumer by eliminating poorly-designed products and processes in addition to spurious advertising.

Given our rising oil imports costs, it is in Australia’s strategic interest to take action to drastically reduce our fuel consumption in passenger and freight transport.

How Australia can dramatically lift its energy productivity across industry sectors is being explored in the Australian Energy Productivity Roadmap.

Can you suggest more? We’d love to hear your thoughts.

Further reading: