The spring budget of 2024 was widely seen as a chance for UK chancellor Jeremy Hunt to inject some economic optimism into British politics ahead of a general election. Would he or wouldn’t he cut income tax? (He wouldn’t.) Would he pull rabbits out of hats in a bid to convince the electorate that the Conservatives should stay in power? Here’s what our panel of experts made of his plans:

National insurance cut only partially offsets rising tax burden

Jonquil Lowe, Senior Lecturer in Economics and Personal Finance, The Open University

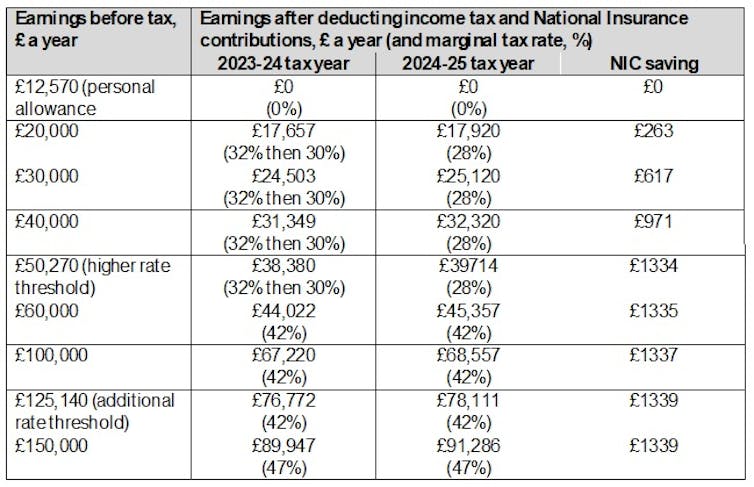

The big attention-grabber in the budget was a two percentage point cut in national insurance contributions for employees and the self-employed from April. It comes hard on the heels of a similar cut in January this year.

The government also announced a long-term, but undated, ambition to abolish national insurance altogether. However, the national insurance cut (which will cost the government £10.1 billion in the coming year) only partially offsets the impact of the ongoing freeze in the income tax personal allowance and higher rate band until April 2028.

Normally these levels would rise each year with inflation. But the freeze causes what’s known as “fiscal drag”, meaning that as your earnings rise, you get drawn into higher tax bands. The higher your top rate of tax (your marginal rate), the less you get to keep of every extra pound you earn.

This amounts to a substantial rise in income tax, estimated to rake in an extra £35 billion a year for the government by 2028-29.

How the national insurance cut might affect you:

Separately, there was good news for better-off parents, with a raising, from April 2024, of the income threshold at which the government starts to claw back the amount the family gets in child benefit. The threshold will rise to £60,000 (from £50,000) and the rate at which the benefit is withdrawn will also be reduced.

The tax charge currently kicks in when the highest earner in the household reaches the threshold, which inherently favours couples. For example, two parents could each earn just under £60,000 (joint earnings of nearly £120,000) and keep their full child benefit. But a single person on £60,000 would start to lose theirs.

The government has said it will look to end this unfairness by asking HMRC to come up with a method of basing the tax charge on household income from 2026.

But this should sound alarm bells. Those with long memories will remember that until 1990, the UK jointly taxed married couples. The introduction of independent taxation was important in giving women independence and privacy in their financial affairs.

But as always with an election year budget, any commitments for the future depend on the outcome of that election. This time next year these matters may not be in Jeremy Hunt’s hands at all.

Why the cuts to national insurance are a damp squib

Shampa Roy-Mukherjee, Vice Dean and Associate Professor in Economics, University of East London

The OBR expects the economy to grow by 0.8% this year and 1.9% next year – that is, 0.5% higher than its autumn forecast. Growth is then forecast to continue this trend until 2027.

The OBR has also forecast that inflation will go back to a 2% target level within the next few months. This means that the key Conservative priorities of tackling inflation and growing the economy are going to be met in 2024.

The chancellor also announced that he has been able to keep to his “fiscal rules” of national debt as a proportion of GDP falling in the next five years, and government borrowing not exceeding 3% of GDP. This will probably reassure the markets that the UK public finances are steady.

The chancellor went into the budget with “fiscal headroom” of approximately £13 billion for pre-election giveaways (though you always want to leave some in reserve for emergency), but he increased this by announcing the reforms to the non-dom tax status. This enabled him to cut employees’ national insurance (NI) by another 2p in the pound, at a cost of £10 billion and benefiting the average worker by £450 a year.

When combined with the NI cut last autumn, the government can now claim to have delivered a £900 annual tax cut to the average worker. Lowering NI might also encourage people to re-enter the workforce or work more, which could boost companies in sectors that have been struggling to attract talent, such as hospitality and manufacturing. However, it might not have a massive impact, given that income tax thresholds remain frozen, meaning more and more workers pay extra tax each year as their wages rise with inflation.

A few bonuses for a few businesses

Hilary Ingham, Professor of Economics, Lancaster University

For all of the expectations around this being the last chance for the government to make its economic case in the year of a general election, this was a rather underwhelming budget.

The main event – a drop in national insurance – was leaked in advance. And aside from that, there was little to get very excited about. Measures directed at UK businesses were rather limited, targeting specific industries and firms of a particular size.

One measure that will be welcomed by owners of small businesses was the VAT threshold being increased from £85,000 to £90,000, meaning that some small firms will be exempt from this tax. But the rise, a mere £5,000, is small.

There was also good news for the hospitality industry, with the freeze on alcohol duty – which had been due to expire – being extended until February 2025. And the pandemic tax relief given to the performing arts industry was made permanent.

Less pleased will be those whose businesses involve letting out holiday properties. The favourable regime they faced, which has been widely blamed for housing shortages in popular areas such as Cornwall and the Lake District, will be abolished.

But perhaps the measure which will have the widest impact for business is that the 5p cut in fuel duty will be maintained, with the duty frozen for a further 12 months. This will be welcomed given the fuel costs that business and households have faced over the last 18 months.

Overall though, for British companies struggling in this harsh economic climate, the news from Jeremy Hunt was rather muted. Tomorrow will be a return to business as usual.

Good vaping measures – shame about the delay

Rob Branston, Senior Lecturer in Business Economics, University of Bath

The new levy on vapes is a win-win-win for society. It is unfortunate that it isn’t due to happen for more than two years, though, as the new measures will only come into force on October 1 2026.

When they arrive, it will lead to higher prices in the shops, which will definitely help to deter the use of these products, particularly for children and young adults, who are amongst the most price sensitive. Action in this area is most welcome as vaping has been increasing greatly in recent years, notably among those who have never smoked, which is worrying as these products are not risk free.

The new tax and associated price increases are probably large enough to make a meaningful difference. A 10ml vaping refill currently costing £2.50 is predicted to increase in cost to £3.70 if nicotine free, and up to £6.10 for the higher nicotine strengths.

These higher prices will be a stronger deterrent if accompanied by restrictions on packaging, flavours, display and availability. The government is planning such restrictions as part of the forthcoming tobacco and vapes Bill. This will create a broad and welcome package of measures, assuming it goes ahead.

One further win is that the levy will bring vapes within the government excise tax system. This should mean more oversight of retailers and manufacturers, which will hopefully make it easier to identify and take action against products that don’t comply with the rules.

Read more: To stop teenagers vaping they need to see it as cringe, not cool

I also welcome the chancellor’s one-off increase in tobacco taxation, which is predicted to increase the cost of a packet of cigarettes by about £0.89. This is a crucial part of the package, since it will help to ensure that e-cigarettes remain a cheaper and less harmful alternative source of nicotine.

The two tax measures together are forecast to increase government tax revenues by £615 million a year by 2028-29, so they will help the government finances at the same time.

Not enough to alleviate fuel poverty

Andrew Burlinson, Lecturer in Economics, University of Sheffield

The recent energy-price crisis caused “epidemic levels” of hardship in the UK, leading the UK to spend £40 billion in energy price support. However, such consumer price support did not target those in most need or protect households from future energy price shocks.

Just under 40% of households (9 million) spend more than 10% of their residual income on energy, after deducting housing costs. Despite prices falling, typical consumers still pay around 60% more than pre-pandemic levels.

The chancellor’s main move to help this situation is to confirm another extension to the £842 million household support fund, which is used at the discretion of local councils to help households struggling with the cost of living. While this fund is potentially more targeted than the price cap and the energy bill support payments, the fact that it doesn’t go directly to those in need means it is probably missed by many households.

Today’s announcement was quiet on reintroducing social tariffs and funding for energy efficiency, suggesting the government has gone cold on these measures since announcing them in the autumn statement 2022. Either form of support could have been funded, at least partly, by the extended windfall tax on oil and gas companies. This apparent U-turn compounds the government’s decision in September to terminate its energy efficiency taskforce.

It risks another decade of low investment into domestic energy efficiency, at a time when UK households are living in some of the leakiest homes in Europe. There’s a clear need for a large-scale rollout of energy efficiency, perhaps by extending the existing requirement on energy companies to insulate the homes of those in fuel poverty.

Not only would this be consistent with the government’s energy-security agenda, it is also widely acknowledged as the key to making energy affordable to consumers for the long term. Despite today’s tax cuts, real incomes have eroded, and many households are struggling to keep their homes warm. Energy debt and arrears rose to record levels from £1.3 billion to £3.1 billion between 2021 and 2024.

This will all have a long-lasting impact on UK households’ physical and mental health. My recent research shows that strengthening households’ resilience to energy price shocks, particularly energy solvency issues, could improve the health and wellbeing of children and adults.

99% mortgages avoided – thankfully

Alper Kara, Professor of Banking and Finance, Brunel University London

The chancellor has cut capital-gains tax charges on the sale of residential property from 28% to 24% for high-income taxpayers. This may bring more supply to the housing market, assuming there are landlords out there who were hesitating to sell due to the higher capital gains payments. If so, many of these properties will be smaller dwellings, which could benefit first-time buyers by bringing down prices.

On the other hand, the change may also encourage potential landlords that wanted to own second properties but did not do so due to high capital gains tax. We will have to wait and see the ultimate impact of the policy on households struggling to get on the mortgage ladder.

Hunt has also abolished tax relief on mortgage payments for furnished holiday lets. The previous regime made holiday-lets more attractive for landlords in comparison to long-term lets. Changing the policy could discourage landlords to convert their properties to holiday lets, which should in turn make more long-term lets available in the market. This will hopefully help households struggling with increasing rental costs.

There were also rumours of the chancellor introducing a 99% mortgages scheme to help first-time-buyers struggling to save enough deposit to buy a home. With such mortgages, households could have bought a home with only a 1% deposit.

It would have been good news for first-time-buyers, though these mortgages would have probably come with higher interest payments as they would have been riskier for banks.

The scheme would also have pushed already inflated UK houses still higher by creating more demand, putting even more pressure on the affordability of mortgages. And such deposits mean a greater risk of home owners ending up in negative equity if house prices drop, meaning the home is not valuable enough to pay off the remainder of the mortgage.

Overall, 99% deposits would have not solved the UK’s chronic housing affordability problem, which many argue is simply because of not building enough new homes. So it’s welcome that the chancellor did not incentivise them.

NHS investment in tech, but what about basic equipment?

Peter Sivey, Reader in Health Economics, Centre for Health Economics, University of York

This budget did not offer any quick solutions for the ongoing NHS crisis. Despite its problems, the NHS has actually seen substantial funding growth in the last few years.

Over the past five years, the official “NHS Long Term Plan” factored in funding increases of 3.4% above inflation from 2019 to 2024. This was interrupted by the pandemic which saw a spike, then a fall, in funding. But the overall goals have been met, with spending now more than £20 billion more in real terms than in 2019.

There are also regular announcements of top-up funding each winter. However, with the long-term plan funding increases coming to an end, the Insitute for Fiscal Studies has noted that existing plans would have seen small but painful real-term cuts to funding in the upcoming financial year.

These have been mitigated by the announcement in the budget of top-up funding of around £2.5 billion in England. But this will see funding essentially flat in real terms, which will feel like a cut in a health service that is treating an expanding and ageing population with increasingly expensive new health technologies.

The chancellor has shown he is not partial to further increases in NHS spending, stating when he was health secretary, that “money alone” was not the solution. That sounds fair enough, but with increasing demands on the NHS, it need real-term rises in spending just to stand still.

The budget also announced a big figure – £3.4 billion – for investment in technology such as improved electronic patient records. However there is already disappointment from within the NHS that this won’t address a more pressing need for more basic investment in equipment and buildings.